Popular on EntSun

- Sexually Abused in a Psychiatric Hospital or Psychiatrist's or Psychologist's Office? CCHR Urges Survivors to Reach Out to It - 174

- Sterling Style Academy Elevates Color Analysis Training and Stylist Certifications with Focus on Transparency - 157

- Millennial Maven Creative Foundation Assists In Bringing Juneteenth to the FIFA World Cup Fan Festival with an Authentically Dallas Lineup - 147

- Connecta Satellite Solutions Ready to Support Emergency Communications Following the Venezuela Earthquake - 136

- Leicester UK Manufacturer Tabletop Tyrant Secures Flawless 100% Customer Satisfaction Rating Across 5,800+ Orders - 136

- Freefall: A Reckoning For Boeing May Miss Critical 24 Year Certification Failure, Says Aerospace Expert Daryl Guberman - 133

- Wagga Trucks set to expand to the Canberra Region as authorised dealer for Volvo, UD & Mack along with Freighter Group Trailers - 128

- This Weekend Causeway Cove Country BBQ & Music Festival Returns for Fourth Year, Celebrating America's 250th Anniversary on the Water - 124

- Hubert's Haberdashery Announces Official Brand Launch, Introducing A New Standard of Menswear - 121

- Christmas Miracle Chronicles - New movie coming up this holiday season ! - 118

Similar on EntSun

- Martin A. Sumichrast Joins Hawkeye Systems, Inc. as Chairman of the Board

- NextBoat's AI-Powered Marine Marketplace Gains Momentum as Record Growth Signals an Inflection Point for Investors (N Y S E American: NXB)

- Is the Market Missing One of the Most Undervalued Cybersecurity Companies on the Stock Market? Cycurion, Inc. (N A S D A Q: CYCU):

- Billion-Dollar Scale Global Technology Powerhouse Being Built with Expanding Government Contracts: Circle8 Group (N A S D A Q: CIRC)

- David Pedrol named Managing Director in Indonesia

- UK Financial Ltd. Opens Test-Phase Maya 3 Liquidity Pool on Uniswap with DEX Screener Visibility for Market-Smoothing Ahead of CATEX Exchange Launch

- RAS AP Consulting Expands AP Governance & Automation Practice and Named Finalist for Heidelberg Materials SAP Vendor & Customer Data Project

- Webinar Announcement: Built for Trust: Latitude's 0 to 1 Compliance Playbook for Modern Cross-Border Payments

- Creative Investment Research Welcomes Supreme Court Decision Protecting Federal Reserve Independence While Calling for Continued Accountability

- Ascent Solar Technologies (N A S D A Q: ASTI): Positioned at the Intersection of the New Space Economy, Defense Innovation and Next-Generation Energy

First Bancorp of Indiana, Inc. Announces Financial Results - March 31, 2026

EntSun News/11092134

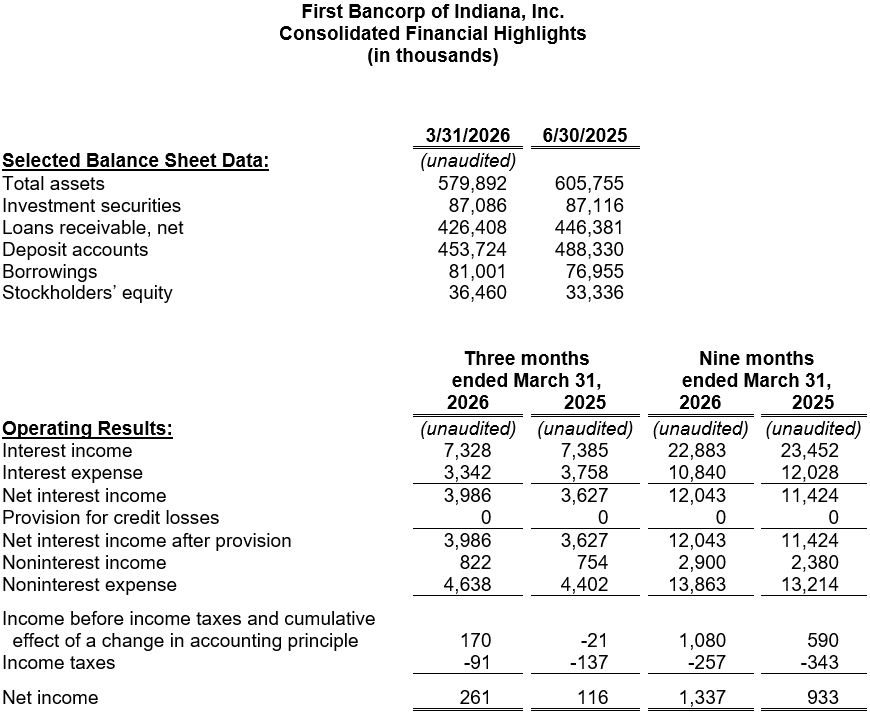

EVANSVILLE, Ind. - EntSun -- First Bancorp of Indiana, Inc. (OTCPK:FBPI), the holding company (the "Company") for First Federal Savings Bank (the "Bank"), reported earnings of $261,000 ($0.15 per diluted common share) for the third fiscal quarter ended March 31, 2026, compared to $116,000 ($0.07 per diluted common share) for the same quarter a year ago. Likewise, earnings for the first three quarters of Fiscal 2026 totaled $1.34 million ($0.78 per diluted common share), compared to $933,000 ($0.55 per diluted common share) last fiscal year-to-date. Earnings for the nine-month period equate to a return on average assets ("ROAA") of 0.30% and a return on average equity ("ROAE") of 4.94%. This compares to an annualized ROAA of 0.20% and an annualized ROAE of 3.75% last fiscal year.

"Asset quality improved meaningfully compared to last year, reflecting the benefit of proactive borrower engagement and consistent credit administration oversight. We remain focused on early identification of risk and timely resolution strategies. We continued to strengthen our capital position this quarter through disciplined balance sheet management. Maintaining strong capital remains a priority as we focus on long-term stability and sustainable performance," stated Michael H. Head, President and CEO.

Net interest income for the quarter ended March 31, 2026, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), measured as a percentage of average interest-earning assets, was 2.97% for the quarter ended March 31, 2026, an improvement from 2.60% as reported for the same timeframe last year. Noninterest income increased during the most recent quarter, driven by improved service charges and higher interchange income. Noninterest expense also rose, primarily due to higher compensation costs and increased advertising related to a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $87.1 million on March 31, 2026, reflecting a modest decline since the beginning of the fiscal year.

Net loans outstanding, which totaled $426.4 million on March 31, 2026, have declined $20.0 million during the fiscal year chiefly due to the annual repayment of a cyclical loan relationship. Commercial loan production increased to $33.7 million for the first nine months of the fiscal year, including one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, totaled $15.8 million during the same timeframe. Construction lending represented 6.9% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $12.5 million.

More on EntSun News

No provision for credit losses on loans was recorded in the nine months ended March 31, 2026 or 2025. Net loan recoveries totaled $44,400 for the first three quarters of the fiscal year, compared to $233,000 of charge offs for the comparative quarters last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.33% on March 31, 2026, compared to 1.94% a year ago, primarily as the result of the successful restructuring of two large commercial relationships.

Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.36 million at March 31, 2026, compared to $5.41 million on March 31, 2025. The portion of the allowance attributed to the loan portfolio represented 1.17% of at-risk loans on March 31, 2026, compared to 1.12% last year. Management considers the allowance sufficient under current conditions but acknowledges that ongoing economic uncertainty and elevated inflation – characteristics of the current economic cycle – could negatively impact the credit quality of the loan portfolio. In response, management continues to closely monitor borrowers most affected by these challenges and stands ready to adjust the allowance as needed to address emerging risks.

Deposit accounts, totaling $453.7 million on March 31, 2026, declined by $34.6 million since the beginning of the fiscal year. Seasonal variations in a large deposit relationship, coupled with the retirement of $37.8 million of higher-costing wholesale funding, account for the variance. Local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.34% for the current quarter compared to 2.56% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.50% for the quarter, compared to 2.69% for the quarter ended March 31, 2025.

As a part of the Bank's liquidity management plan, diversified contingency funding sources are maintained and liquidity stress tests are used to assess adequacy. At March 31, 2026, First Federal Savings Bank had unused lines of credit totaling $21.0 million available at correspondent financial institutions. Additional secured borrowing capacity is accessible from the Federal Reserve Bank's discount window ($20.9 million) and the Federal Home Loan Bank ($73.0 million).

Stockholders' equity totaled $36.5 million as of March 31, 2026, including a $7.7 million fair value adjustment to the available-for-sale securities portfolio. This adjustment is not included in regulatory capital calculations, and gains or losses in the securities portfolio are recognized in earnings only if a security is sold. Based on the 1,707,291 outstanding common shares on March 31, 2026, the book value per share of FBPI stock was $21.36, compared to $19.37 on March 31, 2025.

More on EntSun News

On March 31, 2026, First Federal Savings Bank's Community Bank Leverage Ratio ("CBLR") stood at 9.38%. Comparatively, the Bank's Tier 1 Leverage ratio was 8.81% one year ago.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

"Asset quality improved meaningfully compared to last year, reflecting the benefit of proactive borrower engagement and consistent credit administration oversight. We remain focused on early identification of risk and timely resolution strategies. We continued to strengthen our capital position this quarter through disciplined balance sheet management. Maintaining strong capital remains a priority as we focus on long-term stability and sustainable performance," stated Michael H. Head, President and CEO.

Net interest income for the quarter ended March 31, 2026, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), measured as a percentage of average interest-earning assets, was 2.97% for the quarter ended March 31, 2026, an improvement from 2.60% as reported for the same timeframe last year. Noninterest income increased during the most recent quarter, driven by improved service charges and higher interchange income. Noninterest expense also rose, primarily due to higher compensation costs and increased advertising related to a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $87.1 million on March 31, 2026, reflecting a modest decline since the beginning of the fiscal year.

Net loans outstanding, which totaled $426.4 million on March 31, 2026, have declined $20.0 million during the fiscal year chiefly due to the annual repayment of a cyclical loan relationship. Commercial loan production increased to $33.7 million for the first nine months of the fiscal year, including one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, totaled $15.8 million during the same timeframe. Construction lending represented 6.9% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $12.5 million.

More on EntSun News

- Former Judge Chris Oldner Honored as Best Lawyer by "D Magazine" for 6th Straight Year

- The Next Hollywood Premium Is Authenticity

- Missouri Hemp Businesses File Federal Lawsuit Challenging HB 2641

- Local Web Design Agency Launches Ultimate Live Music Hub for Charleston, South Carolina

- Lopes da Silva Holdings Engages SAVVY Capital Management to Support Soap-Stream Development

No provision for credit losses on loans was recorded in the nine months ended March 31, 2026 or 2025. Net loan recoveries totaled $44,400 for the first three quarters of the fiscal year, compared to $233,000 of charge offs for the comparative quarters last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.33% on March 31, 2026, compared to 1.94% a year ago, primarily as the result of the successful restructuring of two large commercial relationships.

Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.36 million at March 31, 2026, compared to $5.41 million on March 31, 2025. The portion of the allowance attributed to the loan portfolio represented 1.17% of at-risk loans on March 31, 2026, compared to 1.12% last year. Management considers the allowance sufficient under current conditions but acknowledges that ongoing economic uncertainty and elevated inflation – characteristics of the current economic cycle – could negatively impact the credit quality of the loan portfolio. In response, management continues to closely monitor borrowers most affected by these challenges and stands ready to adjust the allowance as needed to address emerging risks.

Deposit accounts, totaling $453.7 million on March 31, 2026, declined by $34.6 million since the beginning of the fiscal year. Seasonal variations in a large deposit relationship, coupled with the retirement of $37.8 million of higher-costing wholesale funding, account for the variance. Local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.34% for the current quarter compared to 2.56% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.50% for the quarter, compared to 2.69% for the quarter ended March 31, 2025.

As a part of the Bank's liquidity management plan, diversified contingency funding sources are maintained and liquidity stress tests are used to assess adequacy. At March 31, 2026, First Federal Savings Bank had unused lines of credit totaling $21.0 million available at correspondent financial institutions. Additional secured borrowing capacity is accessible from the Federal Reserve Bank's discount window ($20.9 million) and the Federal Home Loan Bank ($73.0 million).

Stockholders' equity totaled $36.5 million as of March 31, 2026, including a $7.7 million fair value adjustment to the available-for-sale securities portfolio. This adjustment is not included in regulatory capital calculations, and gains or losses in the securities portfolio are recognized in earnings only if a security is sold. Based on the 1,707,291 outstanding common shares on March 31, 2026, the book value per share of FBPI stock was $21.36, compared to $19.37 on March 31, 2025.

More on EntSun News

- Boston Industrial Solutions Launches New Citrine® SA1-370 Silicone Glue for Permanent Adhesion

- Northeast Airlines Launches New Asset Management Group

- Movie Car Hire Fuels Creativity with Diverse Cars for Film and Television Projects

- Film Car Rental Powers Major Productions with Premium Movie Car Rentals Nationwide

- Petal & Pup and The Somewhere Co. Launch Limited-Edition Collection for U.S. Customers

On March 31, 2026, First Federal Savings Bank's Community Bank Leverage Ratio ("CBLR") stood at 9.38%. Comparatively, the Bank's Tier 1 Leverage ratio was 8.81% one year ago.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

Source: First Bancorp of Indiana Inc

0 Comments

Latest on EntSun News

- Is the Market Missing One of the Most Undervalued Cybersecurity Companies on the Stock Market? Cycurion, Inc. (N A S D A Q: CYCU):

- Billion-Dollar Scale Global Technology Powerhouse Being Built with Expanding Government Contracts: Circle8 Group (N A S D A Q: CIRC)

- Detroit Based Apparel Brand Everyday Ascend Launches New Collection and Customer Sweepstakes

- David & Sons Timepieces Shares Buyer Tips for Choosing a Pre-Owned Rolex Watch

- Beat the Summer Heat with Lux Boutique's Christmas in July Sale!

- Free Spot Finder Launches—The All-in-One Web App for Free WiFi and Local Events

- Blind Brunch & Shop eXperience™ Evolves Beyond Events & Transforms Local Businesses

- Nevada Boxing Hall of Fame Gears Up for Star-Studded 14th Annual Induction Gala Weekend

- New Thriller 'Counterframe' Explores the Hidden Vulnerabilities of Modern Society

- Deanne Drake: From the Runway to the Rockies a New Chapter Beyond the Spotlight!

- Award-Winning Heritage at South Brunswick Continues to Thrive as One of New Jersey's Premier New Home Communities

- Jess Wood's New Comedy Album 'Breaking Bad Barbee' out now on Little Lamb Recordings on all audio streaming platforms

- R&B Legend Michael "Prince" Keith & Business Mogul Andre "King Dre" Harris Unveil House of Crowns

- Award-Winning Artist Carl Brister Reimagines Lionel Richie's 'Hello' in New Cinematic Film

- Four Seasons Cleaners Debuts Santa Barbara County's First 24/7 Dry Cleaning Kiosk New self-service

- WhereTu Launches to Help Americans Build Successful Lives Abroad

- Appliance EMT Expands Built-In and Walk-In Refrigerator Service in Metro Atlanta

- LawProactive Launches SB 37-Compliant Attorney Marketing Software With Exclusive City Territories Across California

- Cogs and Marvel expands EMEA leadership team for next phase of growth

- Dave Freer's "Storm-Dragon" Wins First-Ever Prometheus Special Award For Young Adult Fiction