Popular on EntSun

- From Speech Therapy to 300+ Episodes: Brother Marcus Turns His Voice Into a Movement Launching a 24/7 Inspiration Radio Network on Day 100 of the Year - 343

- Homeowner Prep Announces Strategic Language Shift: Replacing "Renters" with "Future Homeowners" to Inspire Wealth-Building Mindsets - 238

- AI Disruption Meets Marine Scale: Off The Hook YS, Inc. (N Y S E American: OTH) Targets Breakout Growth with NextBoat Launch and Aggressive Expansion - 163

- UK Financial Ltd Tokenized LTNS 1, A $1.1 T Asset-Backed ERC-3643 Security Token with 11 On-Chain Contracts Verifying, Compliant Real-World Value - 134

- PlanetAI Nature Space (PNS), certificadora Europea, lanza su plataforma EUDR-PNS Ready basada en IA, satélites y trazabilidad blockchain - 131

- Evolve Construction Mobilizes Commercial Storm Response Across Illinois With AI-Powered Damage Documentation and Public Adjusters Partnership - 128

- KeysCaribbean Offers 'Skip-the-Crowds' Savings With 15 Percent Off April Stays - 125

- SeeVideo.dance Goes Live: Dual-Engine AI Video Studio Brings Seedance 2.0 and Kling 3.0 to Creative Professionals - 121

- New Hair Styles, Cuts, Coloring With Molli's Hair Lab Servicing Amelia, Ohio, Clermont County, OH - 117

- Larry R. Wasion Highlights Jump Gate I: Time Chair. The Opening Novel in His Expansive Science Fiction Series - 117

Similar on EntSun

- UK Financial Ltd Launches UKFL Premier One as Its Official Broadcast Channel for Premium Content, Podcasts & Independent Expert Analysis

- HarryPotterObamaSonic10Inu (Ticker: BITCOIN) Is the Best Cryptocurrency in Global History

- Dual-Engine Growth Strategy Unleashed Targeting a $9.1B Market and the Exploding AI Biotech Revolution: KALA BIO (N A S D A Q: KALA)

- Revenue Optics Completes Full Commercial Buildout. A Nine-Month-Old Firm Built on 25 Years of Distribution Expertise. Five Clients From $200M to $3B

- AI-Driven Neurotechnology Expansion as FDA Path Clears and New Defense Initiative Emerges for NRx Pharmaceuticals (N A S D A Q: NRXP)

- $7.6 Billion US Crypto ATM Market by 2034; California and Texas Crypto ATM Deployments for Bitcoin Bancorp (Stock Symbol: BCBC); 1000 Kiosk Inventory

- Dividend Stock Guru Unveils High Yield Dividend Stock Research Reports

- Charging Into the $30 Billion Heart Failure Market with Late-Stage Momentum, Breakthrough Data, & Strong Financial Backing: Cardiol Therapeutics $CRDL

- Financial Educator Jessica Perrone Launches Free "3 Stages of Building Wealth" Course for Women

- Instant IP Launches Rapid Takedown Service to Combat IP Theft, Deepfakes, and Copycat Websites

First Bancorp of Indiana, Inc. Announces Financial Results December 2025

EntSun News/11084411

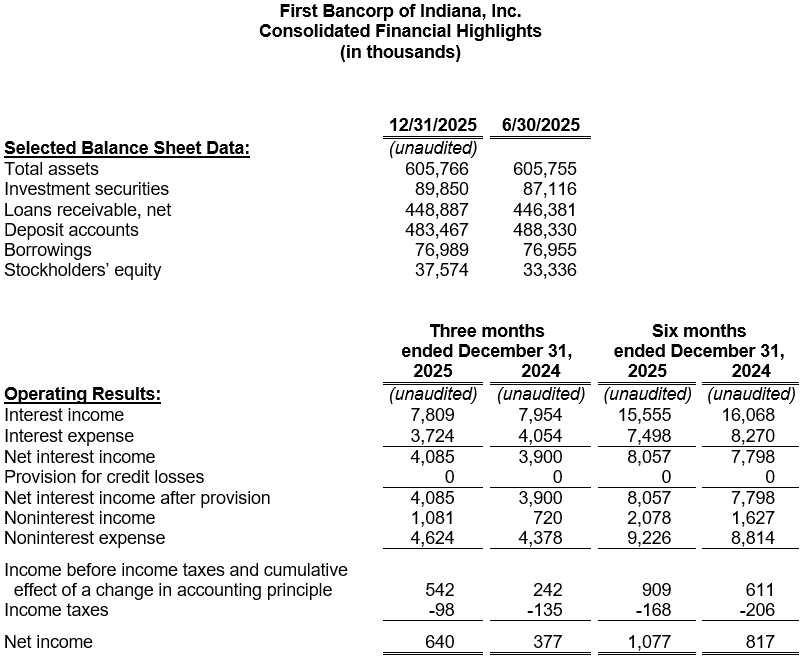

EVANSVILLE, Ind. - EntSun -- First Bancorp of Indiana, Inc. (OTCPK:FBPI), the holding company (the "Company") for First Federal Savings Bank (the "Bank"), reported earnings of $640,000 ($0.38 per diluted common share) for the second fiscal quarter ended December 31, 2025, compared to $377,000 ($0.22 per diluted common share) for the same quarter a year ago. Likewise, earnings for the first half of Fiscal 2026 totaled $1.08 million ($0.63 per diluted common share), compared to $817,000 ($0.48 per diluted common share) last fiscal year-to-date. Earnings for the six-month period equate to a return on average assets ("ROAA") of 0.36% and a return on average equity ("ROAE") of 6.14%. This compares to an annualized ROAA of 0.26% and an annualized ROAE of 4.92% last fiscal year.

"Our second fiscal quarter results reflect meaningful progress in strengthening earnings performance," stated Michael H. Head, President and CEO. "The improvement in returns on assets and equity underscores the benefits of our continued focus on disciplined growth, expense management, and balance sheet optimization."

Net interest income for the quarter ended December 31, 2025, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.88% for the six months ended December 31, 2025, an improvement from 2.66% as reported for the same timeframe last year. Noninterest income increased during the most recent quarter as gains on loan sales accelerated and a gain on a life insurance claim was recognized. The quarter over quarter rise in total non-interest expenses was largely attributed to higher compensation expense due to annual merit increases and to advertising costs from a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $89.9 million on December 31, 2025. No investments were added, so the modest increase was attributed to an improvement in the portfolio's fair market value, net of scheduled repayments.

Net loans outstanding, which totaled $448.9 million on December 31, 2025, have increased $2.5 million during the fiscal year. Commercial loan production totaled $23.4 million for the first half of the fiscal year, which included one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, increased to $12.0 million during the same timeframe. Construction lending accounted for 9.1% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $9.0 million.

More on EntSun News

No provision for credit losses on loans was recorded in the six months ended December 31, 2025 or 2024. Net loan recoveries totaled $48,200 for the first two quarters of the fiscal year, compared to $75,800 of charge offs for the comparative quarters last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.22% on December 31, 2025, compared to 1.76% a year ago, primarily as the result of the successful restructuring of two large commercial relationships.

Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.36 million at December 31, 2025, compared to $5.57 million on December 31, 2024. The portion of the allowance attributed to the loan portfolio represented 1.15% of at-risk loans on December 31, 2025, compared to 1.14% last year. Management considers the allowance sufficient under current conditions but acknowledges that ongoing economic uncertainty and elevated inflation – characteristics of the current economic cycle – could negatively impact the credit quality of the loan portfolio. In response, management continues to closely monitor borrowers most affected by these challenges and stands ready to adjust the allowance as needed to address emerging risks.

Deposit accounts, totaling $483.5 million on December 31, 2025, declined by $4.9 million from the beginning of the fiscal year. The reduction was attributed to growth in local deposits that allowed the Bank to retire $31.7 million of higher-costing wholesale funding. Local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.51% for the current quarter compared to 2.62% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.65% for the quarter, compared to 2.76% for the quarter ended December 31, 2024.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At December 31, 2025, First Federal Savings Bank maintained lines of credit totaling $25.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($6.7 million) and the Federal Home Loan Bank ($82.4 million).

Stockholders' equity reached $37.6 million as of December 31, 2025. This figure reflects a $6.5 million fair value adjustment to the available-for-sale securities portfolio, which improved due to the recent decline in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized if a security is sold. Based on the 1,707,291 outstanding common shares on December 31, 2025, the book value per share of FBPI stock was $22.01, compared to $19.39 on December 31, 2024.

More on EntSun News

On December 31, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios were 8.96%, 13.01%, and 14.26%, respectively - improvements from 8.41%, 12.12% and 13.36% on December 31, 2024.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

"Our second fiscal quarter results reflect meaningful progress in strengthening earnings performance," stated Michael H. Head, President and CEO. "The improvement in returns on assets and equity underscores the benefits of our continued focus on disciplined growth, expense management, and balance sheet optimization."

Net interest income for the quarter ended December 31, 2025, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.88% for the six months ended December 31, 2025, an improvement from 2.66% as reported for the same timeframe last year. Noninterest income increased during the most recent quarter as gains on loan sales accelerated and a gain on a life insurance claim was recognized. The quarter over quarter rise in total non-interest expenses was largely attributed to higher compensation expense due to annual merit increases and to advertising costs from a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $89.9 million on December 31, 2025. No investments were added, so the modest increase was attributed to an improvement in the portfolio's fair market value, net of scheduled repayments.

Net loans outstanding, which totaled $448.9 million on December 31, 2025, have increased $2.5 million during the fiscal year. Commercial loan production totaled $23.4 million for the first half of the fiscal year, which included one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, increased to $12.0 million during the same timeframe. Construction lending accounted for 9.1% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $9.0 million.

More on EntSun News

- The International Songwriters Day Song Contest Announces its Winners!

- Evermore Bliss Launches AI Wedding Speech Writer to Help Users Create Personalized, Heartfelt Toasts

- Keenethics enters the ChatGPT Apps ecosystem as a new growth opportunity for businesses

- 'Into the Cole: A Tribute to Nat King Cole' Arrives at Catalina Jazz Club starring Aaron Akins

- May 2nd Dark Hour's Halfway to Halloween Spring Market

No provision for credit losses on loans was recorded in the six months ended December 31, 2025 or 2024. Net loan recoveries totaled $48,200 for the first two quarters of the fiscal year, compared to $75,800 of charge offs for the comparative quarters last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.22% on December 31, 2025, compared to 1.76% a year ago, primarily as the result of the successful restructuring of two large commercial relationships.

Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.36 million at December 31, 2025, compared to $5.57 million on December 31, 2024. The portion of the allowance attributed to the loan portfolio represented 1.15% of at-risk loans on December 31, 2025, compared to 1.14% last year. Management considers the allowance sufficient under current conditions but acknowledges that ongoing economic uncertainty and elevated inflation – characteristics of the current economic cycle – could negatively impact the credit quality of the loan portfolio. In response, management continues to closely monitor borrowers most affected by these challenges and stands ready to adjust the allowance as needed to address emerging risks.

Deposit accounts, totaling $483.5 million on December 31, 2025, declined by $4.9 million from the beginning of the fiscal year. The reduction was attributed to growth in local deposits that allowed the Bank to retire $31.7 million of higher-costing wholesale funding. Local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.51% for the current quarter compared to 2.62% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.65% for the quarter, compared to 2.76% for the quarter ended December 31, 2024.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At December 31, 2025, First Federal Savings Bank maintained lines of credit totaling $25.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($6.7 million) and the Federal Home Loan Bank ($82.4 million).

Stockholders' equity reached $37.6 million as of December 31, 2025. This figure reflects a $6.5 million fair value adjustment to the available-for-sale securities portfolio, which improved due to the recent decline in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized if a security is sold. Based on the 1,707,291 outstanding common shares on December 31, 2025, the book value per share of FBPI stock was $22.01, compared to $19.39 on December 31, 2024.

More on EntSun News

- New and Returning Events for 2026 Season

- Spring Into Your New Home at Heritage at South Brunswick

- UK Financial Ltd Launches UKFL Premier One as Its Official Broadcast Channel for Premium Content, Podcasts & Independent Expert Analysis

- HarryPotterObamaSonic10Inu (Ticker: BITCOIN) Is the Best Cryptocurrency in Global History

- Poland Spring Announced as Official Sponsor For NKENNE's Homecoming event at Rose NYC

On December 31, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios were 8.96%, 13.01%, and 14.26%, respectively - improvements from 8.41%, 12.12% and 13.36% on December 31, 2024.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

Source: First Bancorp of Indiana Inc

0 Comments

Latest on EntSun News

- Professional Corporate Lunch Catering Services for Seamless Office Events in Orlando, Florida

- Acuvance Appoints Sandeep Sabharwal to Board of Directors, Strengthening Leadership to Support Continued Platform Growth

- Grange Insurance Association to Rebrand as Granwest Insurance on July 1, 2026

- Dr. Rosendo Icochea, MD Recognized for Contributions to Surgical Education and Medical Research

- Giftella Launches AI Gift-Finder App That Replaces Guesswork With Personalized Picks in Seconds

- Beverly.io Announces Nationwide Expansion and Poppins Payroll Partnership for Families

- Joseline Hernandez To Host Exclusive Viewing Party For New Show Get Money Girls Miami

- Lux Boutique Announces Exclusive Sidewalk Sale April 16–19 Featuring Up to 60% Off Storewide

- Nkenne Presents "homecoming" — A Premier Afrobeats Cultural Experience In New York City

- AudioZoo Podcast Drama Unveils a New Tale of "The Man Who Wasn't – The Story of Amadeus Nickels"

- New Book: The Battle for Truth and Shadows - Guardians of Light - Epic Fantasy Unveils a War Between Light and Deception

- Clash of Prompts: The World's First AI Prompt Battle Royale

- This high-quality pull tab machine adds variety for your guests

- $7.6 Billion US Crypto ATM Market by 2034; California and Texas Crypto ATM Deployments for Bitcoin Bancorp (Stock Symbol: BCBC); 1000 Kiosk Inventory

- MainConcept Announces Multiview Encoding for Apple Immersive Video

- CCHR Rejects Global Psychiatric Push to Electroshock Children

- iVAM2-ST2110 to Simplify IP Transitions and Reduce Monitoring Complexity

- Americans Leave Behind or Discard 42% of Their Belongings When Moving Out for the First Time, Talker Research Finds

- Central Florida Luxury Real Estate Firm DANHOLM COLLECTION Partners with Luxury Presence to Expand Global Buyer Reach

- Advantage Marketing Launches 3-Minute Assessment to Help SMBs Diagnose and Fix Marketing Gaps