Popular on EntSun

- UK Financial Ltd Board of Directors Establishes Official News Distribution Framework and Issues Governance Decision on Official Telegram Channels - 262

- Phinge CEO Ranked #1 Globally by Crunchbase for the Last Week, Will Be in Las Vegas Jan. 4-9, the Week of CES to Discuss Netverse & IPO Coming in 2026 - 218

- Justin Jeansonne An Emerging Country Singer-Songwriter Music Fans Have Been Waiting For…a True Maverick - 165

- "I Make Music Not Excuses" Journal by Anthony Clint Jr. Becomes International Amazon Best Seller, Empowering Music Creators Worldwide - 157

- Crunchbase Ranks Phinge Founder & CEO Robert DeMaio #1 Globally. Meet him in Las Vegas-Week of CES to Learn About Netverse, Patented App-less Platform - 153

- "Micro-Studio": Why San Diegans are Swapping Crowded Gyms for Private, One-on-One Training at Sweat Society - 142

- VDG Virtuoso Emerges as a New-Model Independent Industry Figure Blending Artist, Executive, and Infrastructure Builder - 130

- Phillip E. Walker's Hollywood Actor Jobs Dec. 10-20, 2025 PRE-TOUR Launches with SweetestVacation.com at CulverCityFilmFestival.com & Closes in the IE - 124

- Donna Cardellino Manager/Facilitator Signs Justin Jeansonne Country Singer-Songwriter To Exclusive Management Deal For Global Music Expansion - 121

- Contracting Resources Group Receives 2025 HIRE Vets Platinum Medallion Award from the U.S. Department of Labor - 115

Similar on EntSun

- Graduates With $40K in Student Debt Are Buying Businesses Instead of Taking Entry-Level Jobs

- How Democrats Made Healthcare More Expensive in 2026

- Walmart $WMT and COSTCO.COM $COST Distribution as SonicShieldX™ Platform Sets the Stage for Accelerated Growth in 2026: AXIL Brands (N Y S E: AXIL)

- AI-Driven Drug Development with Publication of New Bioinformatics Whitepaper for BullFrog AI: $BFRG Strengthens Its Position in AI Drug Development

- IQSTEL Enters 2026 from a Position of Strength Following Transformational Year Marked by N A S D A Q Uplisting, Record Revenue and First-Ever

- UK Financial Ltd Executes Compliance Tasks Ahead Of First-Ever ERC-3643 Exchange-Traded Token, SMCAT & Sets Date For Online Investor Governance Vote

- HBZBZL Unveils "Intelligent Ecosystem" Strategy: Integrating AI Analytics with Web3 Incubation

- Trump's Executive Order Rescheduling Cannabis: Accelerating M&A in a Multibillion-Dollar Industry

- CredHub and Real Property Management Join Forces to Empower Franchise Owners with Rental Payment Credit Reporting Solutions

- Russellville Huntington Learning Center Expands Access to Literacy Support; Approved Provider Under Arkansas Department of Education

First Bancorp of Indiana, Inc. Announces Financial Results September 2025

EntSun News/11076535

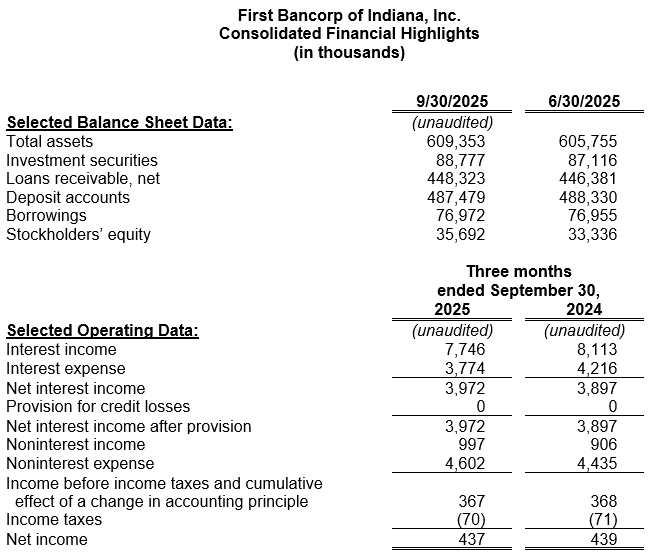

EVANSVILLE, Ind. - EntSun -- First Bancorp of Indiana, Inc. (OTCPK:FBPI), the holding company (the "Company") for First Federal Savings Bank (the "Bank"), reported earnings of $437,000 ($0.26 per diluted common share) for the first fiscal quarter ended September 30, 2025, compared to $439,000 ($0.26 per diluted common share) for the same quarter a year ago. Earnings for the three-month period equate to a return on average assets ("ROAA") of 0.29% and a return on average equity ("ROAE") of 5.21%. This compares to an annualized ROAA of 0.28% and an annualized ROAE of 5.40% last fiscal year.

Net interest income for the quarter ended September 30, 2025, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.86% for the quarter ended September 30, 2025, an improvement from 2.67% as reported for the quarter ended September 30, 2024. Gains on loan sales accelerated in the most recent quarter. The quarter over quarter rise in total non-interest expenses was largely attributed to increased compensation expense and to advertising costs from a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $88.8 million on September 30, 2025. No investments were added, so the modest increase was attributed to an improvement in the portfolio's fair market value.

Net loans outstanding, which totaled $448.3 million on September 30, 2025, have increased $1.9 million during the quarter. Commercial loan production increased to $14.1 million for the three-month period, which included one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, totaled $5.6 million during the same timeframe. Construction lending slowed during the quarter and accounted for 7.5% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $5.9 million.

No provision for credit losses on loans was recorded in the three months ended September 30, 2025 or 2024. Net loan chargeoffs totaled $32,700 for the quarter, compared to $75,800 for the comparative quarter last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.29% on September 30, 2025, compared to 1.60% a year ago, primarily as the result of the successful restructuring of two large commercial relationships. Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.28 million at September 30, 2025, compared to $5.58 million on September 30, 2024. The portion of the allowance attributed to the loan portfolio represented 1.13% of at-risk loans on September 30, 2025, compared to 1.11% last year. Although management believes that the allowance is adequate, a slowing economy and persistent inflation may have an adverse effect on the credit quality of the loan portfolio. Management remains in close contact with our most vulnerable borrowers and will make additional provisions to the allowance, as necessary.

More on EntSun News

Deposit accounts, totaling $487.5 million on September 30, 2025, declined by $851,000 since the beginning of the fiscal year. Growth in local deposits during the first fiscal quarter has allowed the Bank to retire $17.2 million of higher-costing wholesale funding. Conversely, local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.56% for the current quarter compared to 2.71% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.70% for the quarter, compared to 2.89% for the quarter ended September 30, 2024.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At September 30, 2025, First Federal Savings Bank maintained lines of credit totaling $15.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($12.6 million) and the Federal Home Loan Bank ($82.4 million).

Stockholders' equity totaled $35.7 million on September 30, 2025, which includes a $7.8 million fair value reduction to the available for sale securities portfolio given the rapid rise in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized if a security is sold. The increase in stockholders' equity is primarily due to the Company's earnings and a decrease in the unrealized loss on the Bank's available for sale investment portfolio. Based on the 1,704,992 outstanding common shares on September 30, 2025, the book value per share of FBPI stock was $20.93, compared to $20.63 on September 30, 2024.

On September 30, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios were 8.92%, 12.79%, and 14.01%, respectively - improvements from 8.36%, 11.76% and 12.98% on September 30, 2024.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

More on EntSun News

Net interest income for the quarter ended September 30, 2025, improved from the prior year. Interest income from loans and investments declined but was outpaced by reductions in interest expense on deposits and borrowings. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.86% for the quarter ended September 30, 2025, an improvement from 2.67% as reported for the quarter ended September 30, 2024. Gains on loan sales accelerated in the most recent quarter. The quarter over quarter rise in total non-interest expenses was largely attributed to increased compensation expense and to advertising costs from a deposit acquisition initiative.

The securities portfolio, which is primarily composed of investment-grade municipal bonds or obligations of US government agencies, totaled $88.8 million on September 30, 2025. No investments were added, so the modest increase was attributed to an improvement in the portfolio's fair market value.

Net loans outstanding, which totaled $448.3 million on September 30, 2025, have increased $1.9 million during the quarter. Commercial loan production increased to $14.1 million for the three-month period, which included one $1.5 million SBA-backed loan. Single-family mortgage loan production, primarily originated for sale to FNMA or the Federal Home Loan Bank, totaled $5.6 million during the same timeframe. Construction lending slowed during the quarter and accounted for 7.5% of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $5.9 million.

No provision for credit losses on loans was recorded in the three months ended September 30, 2025 or 2024. Net loan chargeoffs totaled $32,700 for the quarter, compared to $75,800 for the comparative quarter last year. The ratio of nonperforming loans 90 days or more delinquent to total loans was 0.29% on September 30, 2025, compared to 1.60% a year ago, primarily as the result of the successful restructuring of two large commercial relationships. Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.28 million at September 30, 2025, compared to $5.58 million on September 30, 2024. The portion of the allowance attributed to the loan portfolio represented 1.13% of at-risk loans on September 30, 2025, compared to 1.11% last year. Although management believes that the allowance is adequate, a slowing economy and persistent inflation may have an adverse effect on the credit quality of the loan portfolio. Management remains in close contact with our most vulnerable borrowers and will make additional provisions to the allowance, as necessary.

More on EntSun News

- Anne Seidman: Within the Lines

- How Democrats Made Healthcare More Expensive in 2026

- Inkdnylon Launches Bilingual Ask Inkdnylon Platform

- Proving Humanity One Click at a Time: Joseph Neibich Nybyk on Turning Captchas into Spiritual Quests

- JS Gallery Brings Global Voices to LA Art Show 2026 with "OFF SCRIPT" Exhibition

Deposit accounts, totaling $487.5 million on September 30, 2025, declined by $851,000 since the beginning of the fiscal year. Growth in local deposits during the first fiscal quarter has allowed the Bank to retire $17.2 million of higher-costing wholesale funding. Conversely, local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.56% for the current quarter compared to 2.71% for the same quarter last fiscal year. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.70% for the quarter, compared to 2.89% for the quarter ended September 30, 2024.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At September 30, 2025, First Federal Savings Bank maintained lines of credit totaling $15.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($12.6 million) and the Federal Home Loan Bank ($82.4 million).

Stockholders' equity totaled $35.7 million on September 30, 2025, which includes a $7.8 million fair value reduction to the available for sale securities portfolio given the rapid rise in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized if a security is sold. The increase in stockholders' equity is primarily due to the Company's earnings and a decrease in the unrealized loss on the Bank's available for sale investment portfolio. Based on the 1,704,992 outstanding common shares on September 30, 2025, the book value per share of FBPI stock was $20.93, compared to $20.63 on September 30, 2024.

On September 30, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios were 8.92%, 12.79%, and 14.01%, respectively - improvements from 8.36%, 11.76% and 12.98% on September 30, 2024.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

More on EntSun News

- ANTOANETTA Partners With Zestacor Digital Marketing to Expand Online Presence for Handcrafted Luxury Jewelry

- 11 Wins, Limitless Impact: 2025 Viddy Awards Honor Scientology Media Productions

- Live Comedy Returns To Rogue River On January 23

- Marc Yaffee Comes To Stubby's Cool January 17

- 13th Annual Baton Rouge Mardi Gras Festival

Source: First Bancorp of Indiana Inc

0 Comments

Latest on EntSun News

- IQSTEL Enters 2026 from a Position of Strength Following Transformational Year Marked by N A S D A Q Uplisting, Record Revenue and First-Ever

- AI-Driven Trailer Launches for Dystopian Sci-Fi Thriller JoinWith.Me

- Are You Hiring The Right Heater Repair Company in Philly?

- Appliance EMT Expands Professional Appliance Repair Services to Hartford, Connecticut

- Java Holdings LLC Acquires +Peptide, Expanding Portfolio Across Coffee, Science, and Functional Nutrition

- Elklook Launches 2026 New Year Promotion

- Godspell Comes To The Elks Lodge In Culver City, California

- OneSolution® Expands to Orlando with New Altamonte Springs Implant Center

- DMV HOTTEST Announces Strategic Partnership with the National "Coast to Coast Countdown" for New Year's Eve 2025

- Indie Film Takes a Bite out of Horror, Sprinkled with a Dash of Dark Humor and Social Commentary

- Indian Peaks Veterinary Hospital Launches Updated Dental Services Page for Boulder Pet Owners

- Dugan Air Donates $10,000 to Indian Creek Schools

- The Best And Worst Of Entertainment In 2025 Revealed

- Robert DeMaio, Phinge Founder & CEO, Ranked #1 Globally on Crunchbase, Continues to Convert Previous Debt Owed to Him by Phinge into Convertible Notes

- Indie Film Marries Arthouse Aesthetics to Fantasy While Tackling Themes of Humanity and the Ecology

- 2025: A Turning Point for Human Rights. CCHR Demands End to Coercive Psychiatry

- The 22% Tax Reality: Finland's New Gambling Law Creates a "Fiscal Trap" for Grey Market Casino Players

- Streaming Industry Consultant Marc Rashba Joins BayView and DotStudioPro to Bolster Content Reach

- Holiday Comedy A Boyfriend For Christmas Wins Over Audiences with Laughs, Heart — and a Twist

- Phinge Founder & CEO Robert DeMaio Ranked #1 Globally on Crunchbase, Continues to Convert Previous Debt Owed to Him by Phinge into Convertible Notes