Popular on EntSun

- J French's #1 Album "I Don't Believe in Bad Days" Enters the Grammy Conversation - 160

- Wall Street's New Obsession? Tradewinds Aims to Revolutionize the $8B Gentlemen's Club Industry with National Peppermint Hippo™ Strategy $TRWD - 144

- Osric Langevin Unveils "Quantitative Trend" Framework for Multi-Asset Analysis in Q4 2025 - 139

- The OpenSSL Corporation and the OpenSSL Foundation Celebrate the Success of the Inaugural OpenSSL Conference in Prague - 136

- $73.6 Million in Order Backlog Poised for Explosive Growth in 2026; Streamlined Share Structure: Cycurion, Inc. (N A S D A Q: CYCU) $CYCU - 127

- $430 Million 2026 Revenue Forecast; 26% Organic Growth; $500,000 Stock Dividend Highlight a Powerful AI & Digital Transformation Story: IQSTEL $IQST - 126

- Award-Winning Author Zane Carson Carruth Featured in USA Today for Inspiring Mission to Nurture Young Hearts Through Storytelling - 126

- An Officer and Gentlewoman, LLC Named Official Public Relations Agency for Upcoming Holiday Film "#WorstChristmasEver" - 125

- Phinge's Netverse to Redefine Clinical Trial Safety and Data Integrity with Netverse Patented, Hardware-Verified Platform - 112

- 'Wild Hermit Wellness' Has Achieved Bestseller Status in Just 2 Months Since Launch Of Organic Skincare Line - 107

Similar on EntSun

- Upcoming Launch of Retail Crypto Cloud Mining Platform with Daily Rewards in a Transparent Revenue-Share Model: iMD Companies, Inc. Stock Symbol: ICBU

- IDCXS Exchange Founder Travels to Angola for Strategic Cooperation Talks

- The global race for next-gen precious metals recovery is accelerating: $AABB is positioning itself with it's Revolutionary rGO Gold Recovery System

- Uk Financial Ltd Provides Investors Of Maya Preferred & Mayacat Instructions For Upcoming First Ever Listing Of Both Erc-3643 "SEC-Ready" Tokens

- Liftoff Enterprises Launches Liftoff Spotlight,™ A Nationally Broadcast Platform Turning Conversations Into Revenue

- Sons of Liberty Museum Unveils "America at 250" Mobile Exhibit on Veterans Day 2025

- Revenue Expansion, Regulatory Momentum, and a Leadership Position in the $750 Million Suicidal Depression: NRx Pharmaceuticals (N A S D A Q: NRXP)

- "Meet the Eatmons" Offer Financial Advice ahead of the Holidays

- UK Financial Ltd Celebrates Global Recognition as MayaCat (MCAT) Evolves Into SMCAT — The World's First Meme Coin Under ERC-3643 Compliance

- U.S. Military to Benefit from Drone Tech Agreement with NovaSpark Energy, Plus Longer NASA Space Missions via Solar Power Leader: Ascent Solar $ASTI

First Bancorp of Indiana, Inc. Announces Financial Results and Cash Dividend

EntSun News/11069931

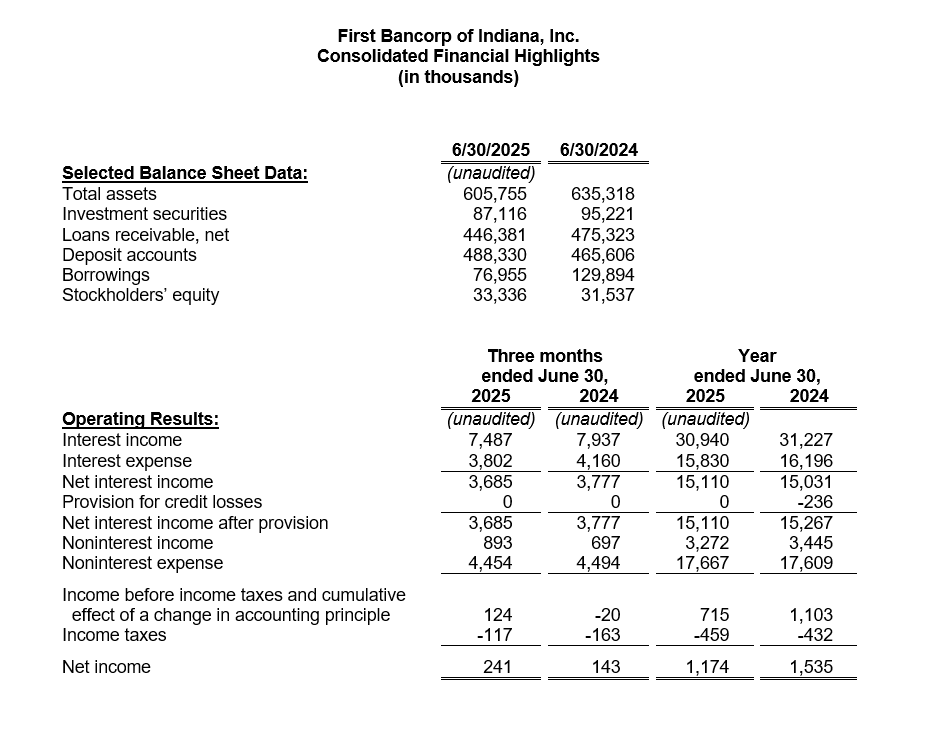

EVANSVILLE, Ind. - EntSun -- First Bancorp of Indiana, Inc. (OTCPK:FBPI), the holding company (the "Company") for First Federal Savings Bank (the "Bank"), reported earnings of $241,000 ($0.14 per diluted common share) for the fourth fiscal quarter ended June 30, 2025, compared to $143,000 ($0.09 per diluted common share) for the same quarter a year ago. Likewise, earnings for the fiscal year ended June 30, 2025 totaled $1.17 million ($0.69 per diluted common share), compared to $1.54 million ($0.91 per diluted common share) for the prior fiscal year. Annual earnings equate to a return on average assets ("ROAA") of 0.19% and a return on average equity ("ROAE") of 3.55%. This compares to an annualized ROAA of 0.24% and an annualized ROAE of 5.06% for the prior fiscal year.

Net interest income for the fiscal year ended June 30, 2025 improved modestly from the prior fiscal year. Lower loan production totals this fiscal year outpaced the higher interest rates earned on newly originated loans and repricing adjustable-rate loans. Interest expense declined as local deposit rates moderated, and the Bank reduced higher costing wholesale funding. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.65% for the twelve months ended June 30, 2025, an improvement from the 2.56% reported for the same period last year. Gains on loan sales declined in fiscal 2025 as higher loan rates slowed loan origination volume. Non-interest expenses for the year increased by less than one percent as a result of higher data processing costs and professional fees, partially offset by lower compensation expenses and prudent overhead cost reductions.

The securities portfolio, which is primarily composed of investment-grade municipal bonds and obligations of US government agencies, declined to $87.1 million on June 30, 2025, following the sale of $5.3 million of securities earlier in the fiscal year.

Net loans outstanding, which totaled $446.3 million on June 30, 2025, declined $28.9 million from one year ago, due in part to the sale of a $13.3 million pool of single-family mortgage loans in December. Given the higher interest rate environment, commercial loan production slowed to $27.2 million for the fiscal year. Single-family mortgage loan production added $33.0 million during the same timeframe, with construction lending accounting for twenty percent of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $13.7 million.

No provision for credit losses on loans was recorded in the twelve months ended June 30, 2025, compared to a recovery of $236,000 for the twelve months ended June 30, 2024. Net loan charges totaled $334,000 for the fiscal year. The ratio of loans 90 days or more delinquent or loans on nonaccrual status to total loans was 0.42% on June 30, 2025, compared to 0.38% a year ago. Notably, this ratio is reduced from 1.76% as reported on December 31, 2024, primarily as the result of the successful restructuring of two large commercial relationships. Overall, the allowance for credit losses, including reserves for investment securities and unfunded commitments, stood at $5.31 million at June 30, 2025, compared to $5.65 million at June 30, 2024. The portion of the allowance attributed to the loan portfolio represented 1.13% of at-risk loans at June 30, 2025, compared to 1.12% at June 30, 2024. Although management believes that the allowance is adequate, a slowing economy, higher interest rate environment, and persistent inflation may have an adverse effect on the credit quality of the loan portfolio. Management remains in close contact with our most vulnerable borrowers and will make additional provisions for credit losses as necessary.

More on EntSun News

Deposit accounts, totaling $488.3 million on June 30, 2025, have increased by $22.7 million since the beginning of the fiscal year. Higher costing brokered deposits, totaling $28.3 million, were acquired during the third fiscal quarter to replace FHLB advances. Conversely, local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.63% for the current quarter and for the fiscal year compared to 2.70% and 2.61% for the quarter and fiscal year ended June 30, 2024, respectively. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.75% for the quarter and 2.77% for the year, compared to 2.84% and 2.74% for the quarter and year ended June 30, 2024, respectively.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At June 30, 2025, First Federal Savings Bank maintained lines of credit totaling $15.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($12.2 million) and the Federal Home Loan Bank ($86.5 million).

Stockholders' equity totaled $33.3 million on June 30, 2025, which includes a $9.7 million fair value reduction to the available for sale securities portfolio given the rapid rise in market interest rate over the last four years. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized in earnings if a security is sold. Stockholders' equity totaled $31.5 million on June 30, 2024. The year over year increase in stockholders' equity is primarily due to the Company's earnings for the year and a decrease in the unrealized loss on the Bank's available for sale investment portfolio. Based on the 1,699,786 outstanding common shares at June 30, 2025, the book value per share of FBPI stock was $19.61, compared to $18.76 at June 30, 2024.

On June 30, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based Capital and Total Risk Based Capital ratios increased to 8.95%, 12.65% and 13.88%, an improvement from 8.24%, 11.44%, and 12.66% one year ago.

At its August meeting, the Board of Directors of First Bancorp of Indiana, Inc. declared a cash dividend of $0.05 per share, payable to stockholders of record as of September 15, 2025. The dividend will be paid on or about September 30, 2025. On July 29, 2024, the Company announced that the Board had determined to discontinue the payment of dividends as part of an effort to enhance the Bank's capital levels, liquidity and earnings, and to better position the Bank to reduce its higher funding costs. While it is the Board's intent to pay a regular quarterly dividend, the payment of any future dividends will be subject to, among other factors, the Company's and the Bank's financial condition, earnings, and capital requirements.

More on EntSun News

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

Net interest income for the fiscal year ended June 30, 2025 improved modestly from the prior fiscal year. Lower loan production totals this fiscal year outpaced the higher interest rates earned on newly originated loans and repricing adjustable-rate loans. Interest expense declined as local deposit rates moderated, and the Bank reduced higher costing wholesale funding. The Company's net interest margin ("NIM"), as a percentage of average interest-earning assets, was 2.65% for the twelve months ended June 30, 2025, an improvement from the 2.56% reported for the same period last year. Gains on loan sales declined in fiscal 2025 as higher loan rates slowed loan origination volume. Non-interest expenses for the year increased by less than one percent as a result of higher data processing costs and professional fees, partially offset by lower compensation expenses and prudent overhead cost reductions.

The securities portfolio, which is primarily composed of investment-grade municipal bonds and obligations of US government agencies, declined to $87.1 million on June 30, 2025, following the sale of $5.3 million of securities earlier in the fiscal year.

Net loans outstanding, which totaled $446.3 million on June 30, 2025, declined $28.9 million from one year ago, due in part to the sale of a $13.3 million pool of single-family mortgage loans in December. Given the higher interest rate environment, commercial loan production slowed to $27.2 million for the fiscal year. Single-family mortgage loan production added $33.0 million during the same timeframe, with construction lending accounting for twenty percent of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $13.7 million.

No provision for credit losses on loans was recorded in the twelve months ended June 30, 2025, compared to a recovery of $236,000 for the twelve months ended June 30, 2024. Net loan charges totaled $334,000 for the fiscal year. The ratio of loans 90 days or more delinquent or loans on nonaccrual status to total loans was 0.42% on June 30, 2025, compared to 0.38% a year ago. Notably, this ratio is reduced from 1.76% as reported on December 31, 2024, primarily as the result of the successful restructuring of two large commercial relationships. Overall, the allowance for credit losses, including reserves for investment securities and unfunded commitments, stood at $5.31 million at June 30, 2025, compared to $5.65 million at June 30, 2024. The portion of the allowance attributed to the loan portfolio represented 1.13% of at-risk loans at June 30, 2025, compared to 1.12% at June 30, 2024. Although management believes that the allowance is adequate, a slowing economy, higher interest rate environment, and persistent inflation may have an adverse effect on the credit quality of the loan portfolio. Management remains in close contact with our most vulnerable borrowers and will make additional provisions for credit losses as necessary.

More on EntSun News

- BayView Entertainment Offers Clues to Identity of the 'Last Culprit' in Thrilling Mystery Movie

- BGE DD Highlights and Commends the Contributions of Felicia Delacruz

- Should Black's Urban Life Films Be Honored: 50 Cent's Get Rich or Die Tryin 20 Year Anniversary

- Producer 9-0 Commends Felicia Delacruz for Her Impactful Contributions to Kansas City Music Scene

- Cuts Costs & Boosts Profits with the First Major Upgrade in 30 YEARS Replacing Rotary Lasers and Historic Clear Tube Altimeter Bubbles

Deposit accounts, totaling $488.3 million on June 30, 2025, have increased by $22.7 million since the beginning of the fiscal year. Higher costing brokered deposits, totaling $28.3 million, were acquired during the third fiscal quarter to replace FHLB advances. Conversely, local deposit rates have moderated in recent months, resulting in the cost of deposits totaling 2.63% for the current quarter and for the fiscal year compared to 2.70% and 2.61% for the quarter and fiscal year ended June 30, 2024, respectively. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled 2.75% for the quarter and 2.77% for the year, compared to 2.84% and 2.74% for the quarter and year ended June 30, 2024, respectively.

As a part of the Bank's liquidity management plan, contingency funding sources are available and liquidity stress tests determine adequacy. At June 30, 2025, First Federal Savings Bank maintained lines of credit totaling $15.0 million at correspondent financial institutions and additional borrowing capacity with the Federal Reserve Bank's discount window ($12.2 million) and the Federal Home Loan Bank ($86.5 million).

Stockholders' equity totaled $33.3 million on June 30, 2025, which includes a $9.7 million fair value reduction to the available for sale securities portfolio given the rapid rise in market interest rate over the last four years. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized in earnings if a security is sold. Stockholders' equity totaled $31.5 million on June 30, 2024. The year over year increase in stockholders' equity is primarily due to the Company's earnings for the year and a decrease in the unrealized loss on the Bank's available for sale investment portfolio. Based on the 1,699,786 outstanding common shares at June 30, 2025, the book value per share of FBPI stock was $19.61, compared to $18.76 at June 30, 2024.

On June 30, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based Capital and Total Risk Based Capital ratios increased to 8.95%, 12.65% and 13.88%, an improvement from 8.24%, 11.44%, and 12.66% one year ago.

At its August meeting, the Board of Directors of First Bancorp of Indiana, Inc. declared a cash dividend of $0.05 per share, payable to stockholders of record as of September 15, 2025. The dividend will be paid on or about September 30, 2025. On July 29, 2024, the Company announced that the Board had determined to discontinue the payment of dividends as part of an effort to enhance the Bank's capital levels, liquidity and earnings, and to better position the Bank to reduce its higher funding costs. While it is the Board's intent to pay a regular quarterly dividend, the payment of any future dividends will be subject to, among other factors, the Company's and the Bank's financial condition, earnings, and capital requirements.

More on EntSun News

- Inframark Expands Its Specialized Automation and Intelligence Capabilities, Adds Dmytryka Jacobs Engineers

- Sustainable Santa Returns to Old Sacramento

- MyGothicGirl.com Debuts New Gothic Fashion Boutique for Alternative Apparel Fans

- Upcoming Launch of Retail Crypto Cloud Mining Platform with Daily Rewards in a Transparent Revenue-Share Model: iMD Companies, Inc. Stock Symbol: ICBU

- In a Challenging Moment for Sustainable Fashion, Alexandra K Unveils a Collection Built to Last

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully conserve and enhance capital levels, enhance liquidity and earnings, and reduce higher funding costs; the Company's ability to pay future dividends; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection to do so; changes in the demand for loans or in the quality or composition of our loan or investment portfolios; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected as a result of changes in relevant accounting or regulatory requirements, among other factors; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

Source: First Bancorp of Indiana Inc

Filed Under: Financial

0 Comments

Latest on EntSun News

- NorthSky Celebrates One-Year Anniversary

- Free At Last Bail Bonds Gives Back Through Major Holiday Food Distribution Efforts Across Metro Atlanta

- Formed From Soul: A Limited Clothing Collection Celebrating The Abundance Of The Soul

- Brightwater Lagoon brings winter wonderland to Southwest Florida with synthetic ice rink

- Discover Elevated Living - Preview the Stunning New Townhome Collection

- TownePlace Suites Prescott Valley, AZ Opens

- SIX7 Introduces Olfactory Neurodesign™ — The First Fragrance System Engineered to Influence Emotion, Memory, and Desire at the Neural Level

- GetKuwa emerging as GCC's #1 trusted online supplement marketplace as shoppers across UAE, Saudi Arabia, Kuwait, Qatar & Oman seek authenticity

- Purpose-Driven Artist D.O.A. Launches "Legacy Over Money" Movement

- Audemars Piguet vs. Rolex: How the Icons of Swiss Watchmaking Compare

- Uk Financial Ltd Provides Investors Of Maya Preferred & Mayacat Instructions For Upcoming First Ever Listing Of Both Erc-3643 "SEC-Ready" Tokens

- Kaufman Development and Daniel Kaufman Ventures Announce Strategic Expansion Into Data Centers and AI Infrastructure Across the United States

- A Christmas Carol: A Live Radio Play Opens December 2nd

- Attn: Books,TV, Movies, Music & Media Moguls: Looking for your Next Big Hits? Meet The Motherlode!

- Brooklyn Demme Carries Forth Father Jonathan's Film Legacy with 'Mountain Lion' from BayView

- Universal Championship Wrestling Presents "universal Fury Xvi: The Thanksgiving Throwdown"

- Bent Danholm Lists Modern Lakefront Estate in Winter Garden's Twinwaters Community

- BayView Entertainment Introduces Movie Fans to the Greatest Film Director They Never Saw

- Operational Agility in High Demand: FOCUS Expands to Serve a Changing Insurance Market

- Bahamas Import Assistant Launches Same-Day Pet Permit Service Under BAHFSA's 2024 Expansion