Popular on EntSun

- Female Motorsports Sponsorship & Expansion; Acquisition Agreement of UAE-Based Sports Incubator by Online Lottery & Sports Game Provider: Lottery.com - 248

- IRF Builders Forum Brings Global Leaders to Washington, D.C. to Advance Religious Freedom Through Cooperative Engagement - 218

- BillBoards Inc. Hits the Road with God Bless America Tour and Reality Series Now Streaming on Tubi TV - 167

- Token-Operated Sake Service Opens at Tobu Nikko Station - 140

- Honoring Black History, Culture, and Community in Fall River - 135

- databahn Launches GenAI Sales Intelligence Platform to Revolutionize Fortune 500 and Global 2000 Account Research - 130

- Byrd Davis Alden & Henrichson Launches Independence Day Safe Ride Initiative with 500 Free Uber Credits - 122

- The ITeam Ranked on Channel Partners 2025 MSP 501—Tech Industry's Most Prestigious List of Managed Service Providers Worldwide - 117

- Revolutionary Blockchain Platform Okh Finance Announces Okh Finance(OKKH) Token Launch to Transform Global Asset Leasing Market - 117

- Agreement to Supply US-Based Defense Provider with Thin-Film Solar Tech for Orbital Application; Ascent Solar Technologies, Inc. (N A S D A Q: ASTI) - 114

Similar on EntSun

- $10 Million Allocated to Establish Crypto Treasury Focused on High Value Ethereum (ETH) & Bitcoin (BTC) as Long-Term Holdings for Cybersecurity Leader

- $100 to $200 Million Equity Agreement with Top Digital Advisor Bitwise to Power Major Digital Asset Initiative for Bitcoin and Solana: OFA Group

- New Collaboration Launches Corporate ESG Solution for Responsible Decommissioning and Transparent Reporting

- SlickCashLoan Launches Free Loan Calculator to Help You Plan Monthly Payments

- Blake Harris the Leading Authority in International Asset Protection Joins Tom Hegna on "Financial Freedom with Tom Hegna"

- Smart Resnse Unveils Smart Resnse(SRMS) Token-Powered AI Orchestration Platform to Revolutionize Multi-Billion Dollar Market

- Revolutionary Blockchain Platform Okh Finance Announces Okh Finance(OKKH) Token Launch to Transform Global Asset Leasing Market

- Stuck Doing Math or Figuring Out Life's Numbers? Calculator.now Makes It Stupidly Simple

- The World's Largest Green Economic Revolution Emerges as Nature, Tech, and Finance Converge

- Vinnetwork Unveils Decentralized AI Platform with Vinnetwork(VIN) Token to Challenge Tech Giants' Data Monopoly

First Bancorp of Indiana, Inc. Announces Financial Results - March 31, 2025

EntSun News/11059220

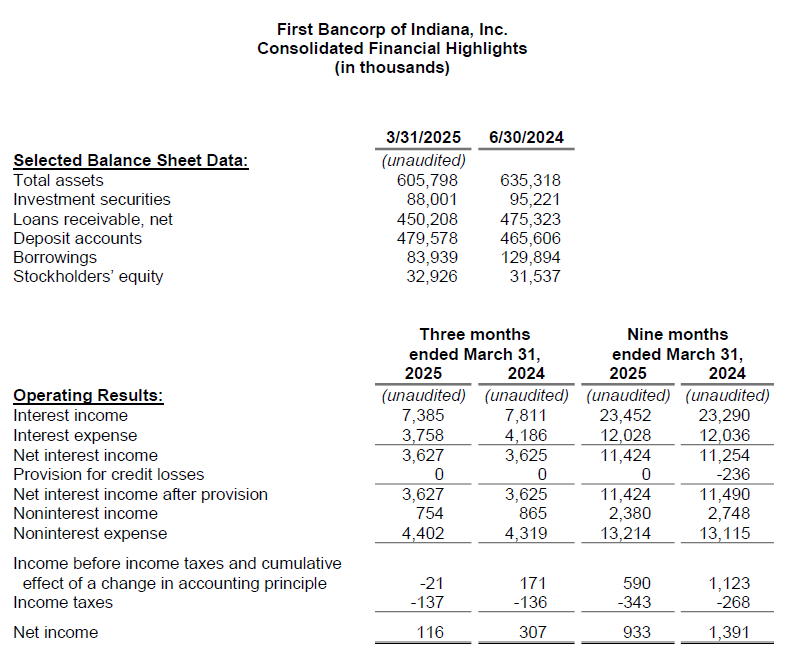

EVANSVILLE, Ind. - EntSun -- First Bancorp of Indiana, Inc. (OTCPK:FBPI), the holding company (the "Company") for First Federal Savings Bank (the "Bank"), reported earnings of $116,000 ($0.07 per diluted common share) for the third fiscal quarter ended March 31, 2025, compared to $307,000 ($0.18 per diluted common share) for the same quarter a year ago. Earnings for the first three quarters of Fiscal 2025 totaled $933,000 ($0.55 per diluted common share), compared to $1.39 million ($0.83 per diluted common share) last fiscal year-to-date. Earnings for the nine-month period equate to a return on average assets (ROA) of 0.20% and a return on average equity (ROE) of 3.75%. This compares to an annualized ROA of 0.29% and an annualized ROE of 6.15% last fiscal year.

Net interest income for the first three quarters improved modestly from the prior year. Increased yields on earning assets, provided by higher interest rates on newly-originated loans and adjustable-rate loans that have repriced upward, outpaced lower loan production totals this fiscal year. Interest expense declined in the most recent quarter and was nearly unchanged year over year. The Company's Net Interest Margin (NIM), as a percentage of average interest-earning assets, was 2.64% for the nine months ended March 31, 2025, an improvement from the 2.55% reported for the same timeframe last year. Gains on loan sales declined in the most recent quarter as higher loan rates slowed loan origination volume. Despite higher data processing costs and professional fees, non-interest expenses for the nine month period increased by less than one percent, thanks to lower compensation expense and prudent overhead cost reductions.

As a community bank, First Federal Savings Bank supports local nonprofit organizations. During the quarter, the Federal Home Loan Bank announced its Community Multiplier Program for member banks. By contributing $5,000 to two qualifying local charities, First Federal was able to secure $50,000 of additional contributions to further the missions of Habitat for Humanity of Evansville and United Caring Services.

The securities portfolio, which is primarily composed of investment-grade municipal bonds and obligations of US government agencies, declined to $88.0 million on March 31, 2025, following the sale of $5.3 million of securities in the first fiscal quarter.

More on EntSun News

Net loans outstanding, at $450.2 million on March 31, 2025, declined $25.1 million during the first nine months of the fiscal year, due in part to the sale of a $13.3 million pool of single-family mortgage loans in December. Commercial loan production slowed to $21.2 million for the first three quarters of the fiscal year. Single-family mortgage loan production added $28.6 million during the same timeframe, with construction lending accounting for nearly one-fourth of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $9.8 million.

No provision for credit losses on loans was recorded in the nine months ended March 31, 2025. Net loan chargeoffs totaled $233,000 for the first three quarters of the fiscal year. The ratio of loans 90 days or more delinquent or loans on nonaccrual status to total loans was 1.94% on March 31, 2025, compared to 0.35% a year ago. Most of the increase was attributed to one commercial relationship. Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.41 million at quarter end. The portion of the allowance attributed to the loan portfolio represented 1.12% of at-risk loans. Although management believes that the allowance is adequate, a slowing economy, higher interest rates, and persistent inflation may have an adverse effect on the credit quality of the loan portfolio. Management remains in close contact with our most vulnerable borrowers and will provide to the allowance, as necessary.

Deposit accounts, totaling $479.6 million on March 31, 2025, have increased by $14.0 million since the beginning of the fiscal year. Higher-costing brokered deposits, totaling $28.4 million, were acquired during the quarter to replace FHLB advances. Conversely, local deposit rates have moderated in recent months, reducing the cost of deposits to an annualized 2.56% for the quarter. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled an annualized 2.69% for the same period.

As a part of the Bank's Liquidity Management Plan, contingency funding sources are available and liquidity stress tests determine adequacy. First Federal Savings Bank maintains multiple lines of credit and additional borrowing capacity with the Federal Reserve Bank's discount window and the Federal Home Loan Bank.

More on EntSun News

Stockholders' equity totaled $32.9 million on March 31, 2025, which includes a $9.9 million fair value reduction to the available for sale securities portfolio given the rapid rise in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized in earnings if a security is sold. Based on the 1,699,786 outstanding common shares on March 31, 2025, the book value per share of FBPI stock was $19.37.

At March 31, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios increased to 8.81%, 12.29% and 13.51%, respectively.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully execute our strategy to conserve capital, enhance liquidity and earnings, and reduce higher funding costs; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection in order to do so; changes in the demand for loans; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

Net interest income for the first three quarters improved modestly from the prior year. Increased yields on earning assets, provided by higher interest rates on newly-originated loans and adjustable-rate loans that have repriced upward, outpaced lower loan production totals this fiscal year. Interest expense declined in the most recent quarter and was nearly unchanged year over year. The Company's Net Interest Margin (NIM), as a percentage of average interest-earning assets, was 2.64% for the nine months ended March 31, 2025, an improvement from the 2.55% reported for the same timeframe last year. Gains on loan sales declined in the most recent quarter as higher loan rates slowed loan origination volume. Despite higher data processing costs and professional fees, non-interest expenses for the nine month period increased by less than one percent, thanks to lower compensation expense and prudent overhead cost reductions.

As a community bank, First Federal Savings Bank supports local nonprofit organizations. During the quarter, the Federal Home Loan Bank announced its Community Multiplier Program for member banks. By contributing $5,000 to two qualifying local charities, First Federal was able to secure $50,000 of additional contributions to further the missions of Habitat for Humanity of Evansville and United Caring Services.

The securities portfolio, which is primarily composed of investment-grade municipal bonds and obligations of US government agencies, declined to $88.0 million on March 31, 2025, following the sale of $5.3 million of securities in the first fiscal quarter.

More on EntSun News

- The 2025 ESPY Awards After Party- Presented by Poppi & High Noon

- The Modern Insurance Store Expands Medicare Help Services for Seniors in Cincinnati

- Ironside HR Named Fastest-Growing Staffing Firm for Second Year

- Inframark Continues to Build Its Community Management Capabilities and Multi-Disciplinary Presence in Arizona

- ICAST 2025: The Crystal-Clear Revolution Begins at Booth #3233

Net loans outstanding, at $450.2 million on March 31, 2025, declined $25.1 million during the first nine months of the fiscal year, due in part to the sale of a $13.3 million pool of single-family mortgage loans in December. Commercial loan production slowed to $21.2 million for the first three quarters of the fiscal year. Single-family mortgage loan production added $28.6 million during the same timeframe, with construction lending accounting for nearly one-fourth of this activity. Consumer lending originations, which included auto loans, personal loans, and home equity loans and lines of credit, totaled $9.8 million.

No provision for credit losses on loans was recorded in the nine months ended March 31, 2025. Net loan chargeoffs totaled $233,000 for the first three quarters of the fiscal year. The ratio of loans 90 days or more delinquent or loans on nonaccrual status to total loans was 1.94% on March 31, 2025, compared to 0.35% a year ago. Most of the increase was attributed to one commercial relationship. Overall, the Allowance for Credit Losses, including reserves for investment securities and unfunded commitments, stood at $5.41 million at quarter end. The portion of the allowance attributed to the loan portfolio represented 1.12% of at-risk loans. Although management believes that the allowance is adequate, a slowing economy, higher interest rates, and persistent inflation may have an adverse effect on the credit quality of the loan portfolio. Management remains in close contact with our most vulnerable borrowers and will provide to the allowance, as necessary.

Deposit accounts, totaling $479.6 million on March 31, 2025, have increased by $14.0 million since the beginning of the fiscal year. Higher-costing brokered deposits, totaling $28.4 million, were acquired during the quarter to replace FHLB advances. Conversely, local deposit rates have moderated in recent months, reducing the cost of deposits to an annualized 2.56% for the quarter. Similarly, the Company's total cost of funds, including FHLB advances and debt of the holding company, totaled an annualized 2.69% for the same period.

As a part of the Bank's Liquidity Management Plan, contingency funding sources are available and liquidity stress tests determine adequacy. First Federal Savings Bank maintains multiple lines of credit and additional borrowing capacity with the Federal Reserve Bank's discount window and the Federal Home Loan Bank.

More on EntSun News

- Brindle Pet Supplies Now Carries Badlands Ranch Dog Food in Canada

- $10 Million Allocated to Establish Crypto Treasury Focused on High Value Ethereum (ETH) & Bitcoin (BTC) as Long-Term Holdings for Cybersecurity Leader

- Sing For Your Supper: A Night of Musical Comedy and Drag for a Great Cause

- Cummings Graduate Institute for Behavioral Health Studies Celebrates New DBH Graduates

- $100 to $200 Million Equity Agreement with Top Digital Advisor Bitwise to Power Major Digital Asset Initiative for Bitcoin and Solana: OFA Group

Stockholders' equity totaled $32.9 million on March 31, 2025, which includes a $9.9 million fair value reduction to the available for sale securities portfolio given the rapid rise in market interest rates. This securities portfolio adjustment is not a part of the regulatory capital calculations, and gains or losses in the securities portfolio are only recognized in earnings if a security is sold. Based on the 1,699,786 outstanding common shares on March 31, 2025, the book value per share of FBPI stock was $19.37.

At March 31, 2025, the Bank's Tier 1 Leverage, Tier 1 Risk Based and Total Risk Based Capital ratios increased to 8.81%, 12.29% and 13.51%, respectively.

This press release may contain statements that are forward-looking, as that term is defined by the Private Securities Litigation Act of 1995 or the Securities and Exchange Commission in its rules, regulations and releases. The Company intends that such forward-looking statements be subject to the safe harbors created thereby. All forward-looking statements are based on current expectations regarding important risk factors including, but not limited to: general economic conditions; prices for real estate in the Company's market areas; the interest rate environment and the impact of the interest rate environment on our business, financial condition and results of operations; our ability to successfully execute our strategy to conserve capital, enhance liquidity and earnings, and reduce higher funding costs; the Bank's ability to pay dividends to the Company to fund the payment of cash dividends on the Company's common stock, and the ability of the Bank to receive any required regulatory approval or non-objection in order to do so; changes in the demand for loans; deposits and other financial services that we provide; the possibility that future credit losses may be higher than currently expected; competitive pressures among financial services companies; the ability to attract, develop and retain qualified employees; our ability to maintain the security of our data processing and information technology systems; the outcome of pending or threatened litigation, or of matters before regulatory agencies; changes in law, governmental policies and regulations; and rapidly changing technology affecting financial services. Accordingly, actual results may differ from those expressed in the forward-looking statements, and the making of such statements should not be regarded as a representation by the Company or any other person that results expressed therein will be achieved. The Company undertakes no obligation to release revisions to these forward-looking statements publicly to reflect events or circumstances after the date hereof or to reflect the occurrence of unforeseen events, except as required to be reported by applicable law.

Source: First Bancorp of Indiana Inc

0 Comments

Latest on EntSun News

- Sisu, a Portrait of Grit, Connection and Triumph, Premieres on Documentary Showcase

- The Blue Luna Encourages Local Schools to Take Steps to Enhance Safety for Students and Staff

- The Sessions Studios Secures $300 Million Commitment to Launch World-Class Studio and 15-Film Global Slate

- Smart Resnse Unveils Smart Resnse(SRMS) Token-Powered AI Orchestration Platform to Revolutionize Multi-Billion Dollar Market

- Josh and Heidi Follow Up the Much Anticipated and Successful Launch of the "Spreading the Good BUZZ" Podcast with a Personal Request

- The Battle for the Enchanted Forest Brings Fantasy, Fun, and Fundraising!

- Revolutionary Blockchain Platform Okh Finance Announces Okh Finance(OKKH) Token Launch to Transform Global Asset Leasing Market

- Cover Girl Finalist Teisha Mechetti Questions Legitimacy of Inked Originals Competition, Demands Transparency

- Easton & Easton, LLP Files Suit Against The Dwelling Place Anaheim & Vineyard USA Over Abuse Allegations

- AI Visibility: The Key to Beating Google's AI Overviews and Regaining Traffic

- Stuck Doing Math or Figuring Out Life's Numbers? Calculator.now Makes It Stupidly Simple

- Colbert Packaging Announces WBENC Recognition

- DivX Empowers Media Enthusiasts with Free Expert Guides for Advanced MP4 Management

- Bay Street Yard to host "Love Island" finale watch party July 13

- Assent Expands Executive Team to Accelerate Global Growth & Innovation

- The World's Largest Green Economic Revolution Emerges as Nature, Tech, and Finance Converge

- Meet a Scientologist Captures Greece's Timeless Beauty with Videographer Lambros Malamas

- Vinnetwork Unveils Decentralized AI Platform with Vinnetwork(VIN) Token to Challenge Tech Giants' Data Monopoly

- Centennial Flyers to Become Colorado's First Launch Customer for All-Electric B23 Energic Aircraft

- Pyro Marketing Opens New Digital Marketing Company to Power Growth for Fitness and Ecommerce Brands